The NZD/USD pair is exhibiting a dominant bearish bias with medium analytical confidence, as a strong higher-timeframe downtrend on the daily and four-hour charts transitions into a temporary short-term intraday consolidation. This technical pause reflects near-term exhaustion and oversold conditions, leaving the pair highly sensitive to upcoming high-impact US economic data. While New Zealand's structural dairy export sector provides a long-term fundamental cushion, the immediate macroeconomic backdrop is dominated by collapsing RBNZ rate hike bets, weak domestic growth indicators, and the Federal Reserve's persistent yield advantage. The tension between these medium-term supportive commodities and immediate cyclical headwinds caps overall analytical confidence, keeping the pair bound to its immediate technical ranges ahead of critical US inflation and growth catalysts.

Technical Analysis

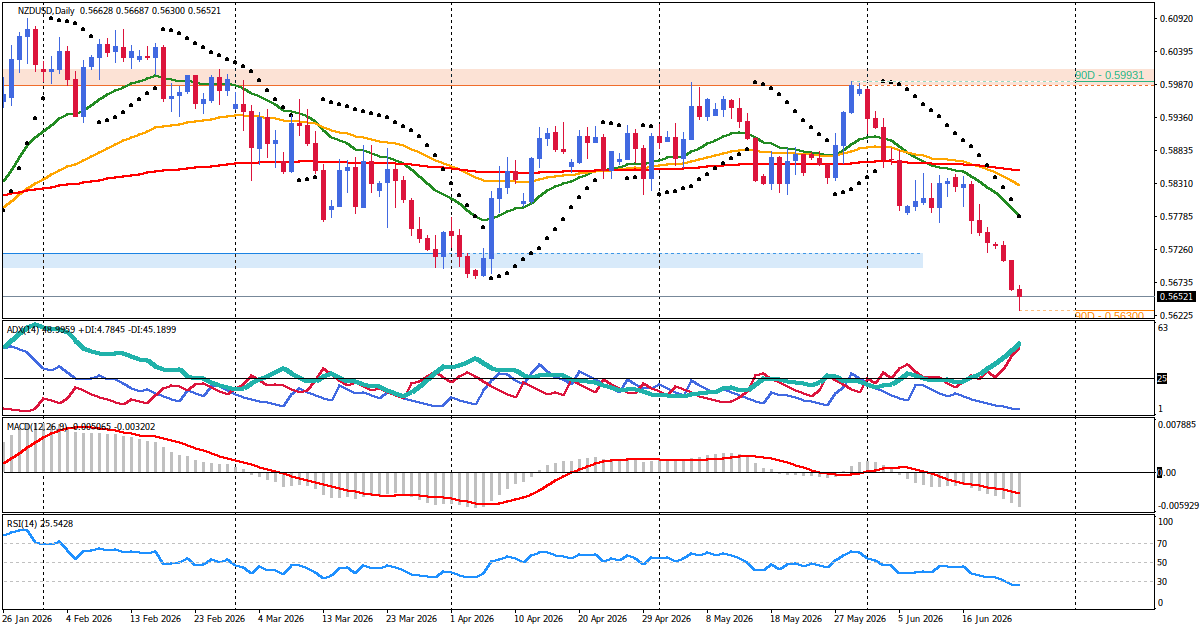

The technical structure of NZD/USD remains heavily bearish across major timeframes, though short-term price action indicates a state of temporary consolidation and seller exhaustion. On the daily (D1) chart, the primary trend is firmly downward, characterized by a persistent sequence of lower highs and lower lows following the breakdown below the key April low of 0.5678. This breakdown confirms the resumption of the broader decline from the January peak of 0.6092, shifting focus toward deeper support targets. However, daily momentum is deeply oversold, and volatility is contracting as price compresses, warning of potential near-term exhaustion.

The medium-term four-hour (H4) framework aligns with this bearish outlook, displaying a strong downward trend but with highly stretched momentum. This suggests that the immediate downward impulse may have run its course, necessitating a consolidation period to digest recent losses before further extensions can materialize. Consequently, the short-term intraday charts (H1 and M30) have transitioned into a mixed, flat structure, establishing a horizontal trading range. Volatility is expanding on these lower timeframes as price tests the upper and lower boundaries of this consolidation zone. This temporary intraday range conflicts with the dominant bearish higher-timeframe trend, keeping immediate tactical setups confined to range-bound behaviors until a clear structural breakout occurs.

Key Price Levels

- Resistance Zone 1 (0.5658 to 0.5663): Formed by the H1 upper Bollinger Band and the daily lower Bollinger Band limit, serving as the immediate ceiling for intraday bounces.

- Resistance Zone 2 (0.5685 to 0.5690): Aligned with the H4 EMA20 and the H4 middle Bollinger Band.

- Resistance Zone 3 (0.5735 to 0.5740): A major structural zone containing the H4 EMA50 and the H1 EMA200 cluster. Additionally, the broader level of 0.5768 (former support turned resistance) remains a critical medium-term pivot.

- Support Zone 1 (0.5630 to 0.5636): Defined by recent H4 and H1 swing lows, acting as the immediate floor of the consolidation range.

- Support Zone 2 (0.5620 to 0.5625): Based on the H4 lower Bollinger Band.

- Support Zone 3 (0.5600 to 0.5610): A psychological level confluence, closely preceding the critical medium-term support cluster at 0.5580, which represents the 100% projection of the 0.6092 to 0.5678 move from 0.5993.

Fundamental Drivers

The fundamental backdrop presents a stark divergence between long-term structural supports and immediate cyclical headwinds. Structurally, the New Zealand Dollar is anchored by robust global dairy prices. Consecutive Global Dairy Trade (GDT) events have shown broad-based gains, prompting Fonterra to forecast an elevated farmgate milk price of $13.00 to $15.00 per kgMS for the 2026/27 season. This is backed by Stats NZ overseas trade data, which highlighted an 18% year-on-year increase in dairy export values.

However, these structural positives are currently being overwhelmed by a dramatic shift in domestic monetary policy expectations and growth concerns. Speculation of a near-term Reserve Bank of New Zealand (RBNZ) rate hike has collapsed. Previously, geopolitical tensions in the Middle East and rising oil prices had fueled fears of imported inflation, leading markets to price in a potential RBNZ rate hike as early as July. The subsequent US-Iran ceasefire and sharp drop in global crude prices have completely defused this inflation urgency. Simultaneously, weak domestic economic indicators—including contracting Manufacturing and Services PMIs and downbeat Q2 GDP forecasts—have forced market participants to price out tightening, with expectations shifting to the RBNZ remaining on hold at 2.25%. This dovish repricing, contrasted against the Federal Reserve's higher policy rate of 3.50% to 3.75%, maintains a persistent yield disadvantage for the Kiwi, reinforcing the bearish technical pressure on the NZD/USD.

Market Sentiment and Risk Environment

Global market sentiment has turned increasingly risk-averse, further weighing on the risk-sensitive New Zealand Dollar. A wave of deleveraging across global equity markets, particularly within the technology sector, has prompted investors to scale back exposure to growth-linked and high-beta assets. In this environment, the US Dollar has actively benefited from capital preservation flows and safe-haven demand. This risk-off tone directly challenges the commodity-linked support of the NZD, as carry-trade dynamics and growth-oriented assets face liquidation, amplifying the yield-based appeal of the Greenback.

Primary Scenario

The primary scenario is a bearish continuation of the dominant higher-timeframe trend, following the resolution of the current intraday consolidation. This path is favored by the combination of technical trend alignment and the macroeconomic yield disadvantage. The structural trigger for this move is a sustained break below the immediate support at 0.5630. Confirmation requires a closed H1 candle below this level, followed by a successful retest of the zone as resistance. Under this scenario, price action is expected to extend downward toward Support Zone 2 (0.5620 to 0.5625) and eventually target the critical medium-term support cluster at 0.5580. This scenario would be invalidated if the pair achieves a strong hourly close above the H1 EMA20 at 0.5648, indicating prolonged range-bound behavior or a deeper corrective pullback.

Alternative Scenario

The alternative scenario outlines a corrective technical pullback, driven by the deeply oversold conditions on the daily and four-hour charts. This scenario would be triggered by a clear, high-volume breakout above the immediate resistance at 0.5663. Confirmation requires a strong H1 candle close above this level, establishing a structural shift on the lower timeframes. The resulting upward correction would target Resistance Zone 2 (0.5685 to 0.5690), with potential extension toward the 0.5735 to 0.5740 area. This corrective rally is highly dependent on upcoming economic catalysts, specifically weaker-than-expected US Core PCE or GDP data, which would temporarily alleviate upward pressure on the US Dollar. A break and close below 0.5630 would immediately invalidate this corrective outlook, reinstating the primary bearish trend.

Economic Calendar and Catalysts

The active trading window contains several high-impact scheduled catalysts capable of driving significant volatility and breaking the current intraday consolidation:

- June 25, 01:30 UTC - Australian Employment Change & Unemployment Rate: As a key regional economic indicator, Australian labor data frequently triggers sympathy volatility across Antipodean pairs, directly impacting New Zealand Dollar sentiment. The market forecasts an employment change of 31.2K and an unemployment rate of 4.4%.

- June 25, 12:30 UTC - United States Core PCE Price Index & Final GDP: These pivotal inflation and economic growth metrics serve as the primary macro catalysts for the US Dollar. The Core PCE is expected to print at 0.3% month-on-month, while Final GDP is projected at 1.6% quarter-on-quarter. Stronger-than-expected figures would reinforce the Fed's higher-for-longer rate stance, while a soft print could trigger a sharp corrective bounce in NZD/USD.

- June 25, 12:30 UTC - United States Unemployment Claims: Released alongside GDP and PCE, weekly claims (forecast at 225K) will provide high-frequency updates on the US labor market.

- June 26, 14:00 UTC - US Revised University of Michigan Consumer Sentiment: This release (forecast at 50.0) and its accompanying inflation expectations will help shape late-week sentiment and USD momentum.

Outlook

The short-term outlook for NZD/USD points to a state of high-stakes consolidation with an underlying bearish bias. While the primary and medium-term trends are heavily aligned to the downside, the extreme oversold conditions and contracting volatility on the daily timeframe suggest that the path of least resistance may involve further range-bound consolidation before the broader downtrend resumes. The primary confidence limiter remains the tension between the long-term, supportive dairy export fundamentals and the immediate cyclical headwinds of fading RBNZ hike expectations and a strong US yield advantage. Ultimately, the resolution of this technical pause hinges on the upcoming US PCE and GDP releases, which will dictate whether the pair breaks lower toward the critical 0.5580 support cluster or initiates a corrective pullback toward key overhead resistance zones.

Disclaimer: This is not personalized financial advice. The information is for educational purposes only and does not guarantee any future outcome.